GDR Model Review: April 2025

10%+ returns amidst highest volatility since 2020

The GDR Model returned 10.87% vs the S&P 500’s Total Return of -0.68%, beating the index by 1,115 basis points in April.

The GDR Model is up 24.77% as of the end of April 2025 compared with the S&P 500’s Total Return of -4.92%. The model is ahead by 2,969 basis points.

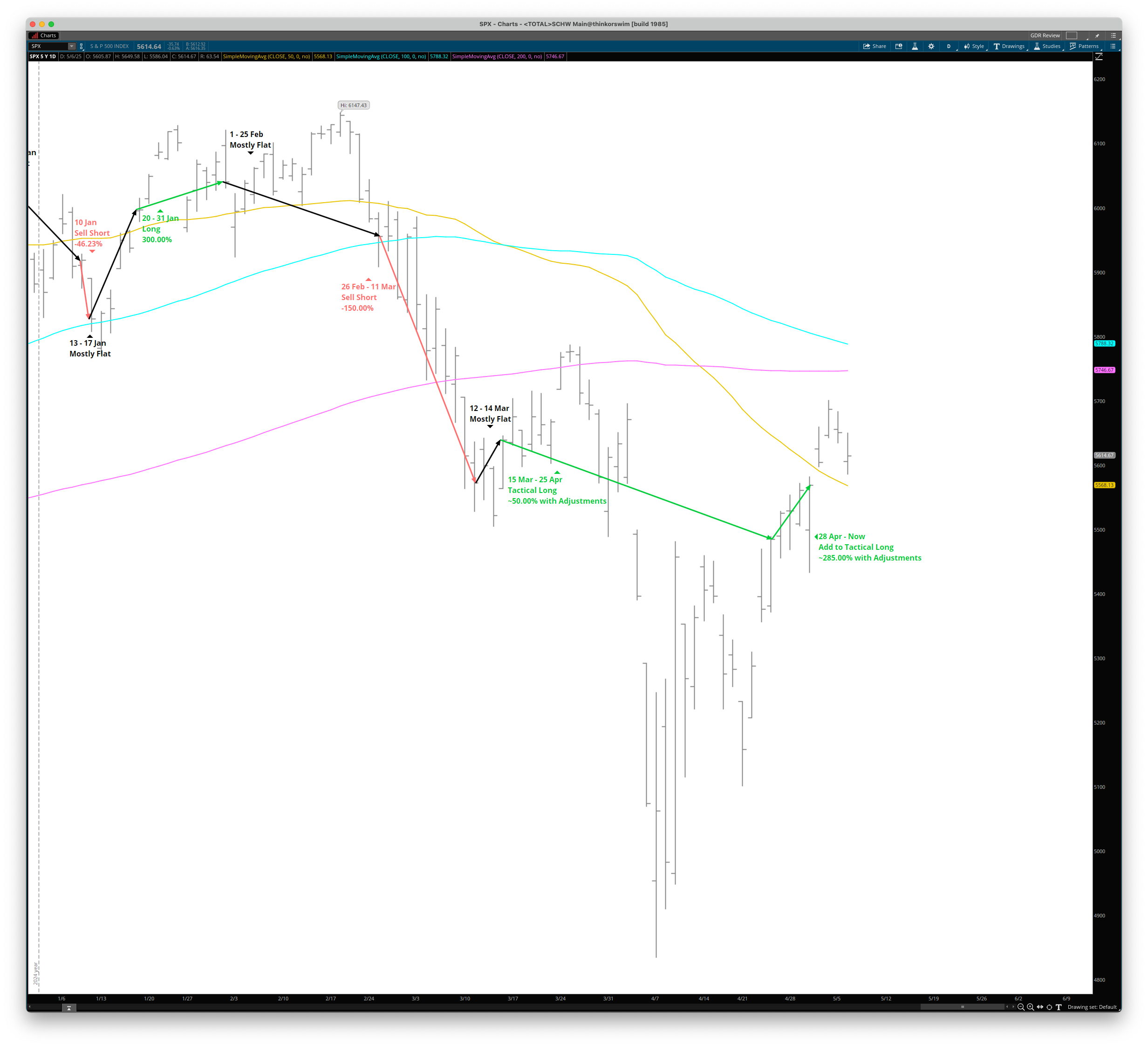

The model started out the month holding the tactical long at around 50% of the portfolio’s value, which was carried over from mid-March.

This might not have been the easiest position to hold through all the volatility this month, but the logic is that valuations were cheap enough that holding a long position made sense.

It’s a tactical position that the model will put on from time to time that tends to take partial profits after a profitable day and add back to the position after a losing one.

Towards the end of the month the GDR Model boosted the tactical long to 285% as it noted a strong improvement in market conditions. This position was held into May.

Overall the GDR Model continues to work as intended. While ideally it would have captured the massive drop at the start of the month with a short position, realistically those are difficult situations for an algorithmic model. Instead, we’ve opted for a more realistic process of building a long position when valuations are favorable.